What is SafeWithdrawls?

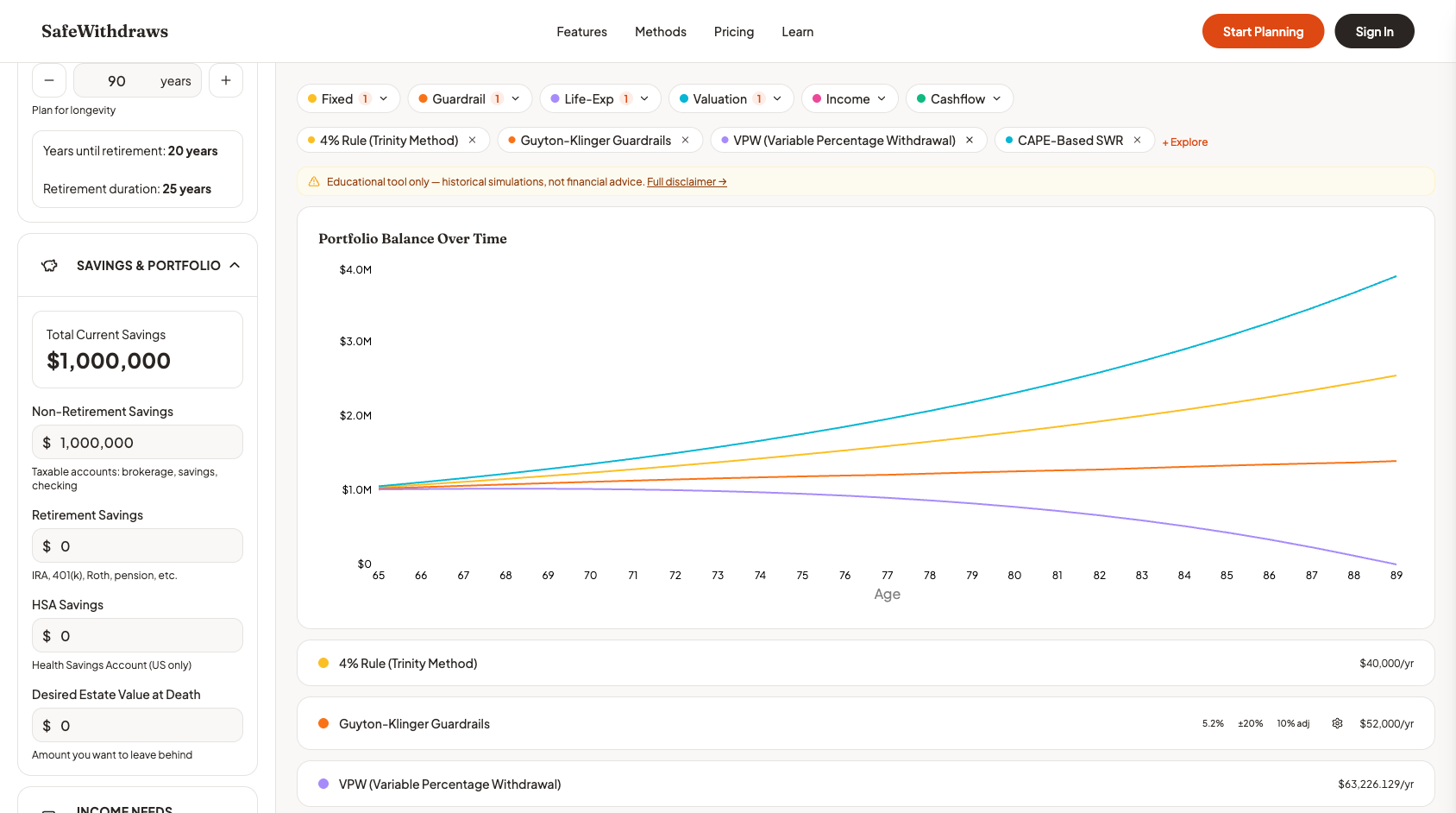

SafeWithdrawls is an educational tool that helps you compare 23 retirement withdrawal strategies side-by-side. Instead of guessing which approach might work best for your situation, you can model multiple methods against realistic market conditions and see exactly how each one performs over a 30+ year retirement.

The Problem We Solve

Choosing a withdrawal strategy is one of the most consequential decisions retirees face. The classic "4% Rule" is a starting point, but it is only one of dozens of approaches -- and it may not be the best fit for your specific situation, risk tolerance, or income needs.

Most planning tools let you test one strategy at a time. SafeWithdrawls lets you compare many strategies simultaneously, so you can see the trade-offs between them in a single view.

23 Methods Across 6 Categories

Every withdrawal strategy makes different assumptions about how to balance longevity risk against lifestyle needs. SafeWithdrawls organizes its 23 methods into six categories based on their core approach:

| Category | Approach | Example Methods |

|---|---|---|

| Fixed-Rate | Withdraw a set amount or percentage each year | Fixed Dollar, 4% Rule, Fixed Percentage |

| Guardrail-Dynamic | Adjust withdrawals based on portfolio performance | Guyton-Klinger, Floor-Ceiling, Ratcheting |

| Life-Expectancy | Scale withdrawals to remaining life expectancy | VPW, RMD, ARVA |

| Valuation-Based | Adjust based on market valuations like CAPE ratio | CAPE-Based, Valuation-Informed, Bond Yield Plus |

| Income-Coordinated | Coordinate with Social Security, annuities, or pensions | SS Bridge, Annuity Hybrid, Prime Harvesting |

| Cashflow-Matching | Match specific expenses to dedicated asset pools | Bucket, Bond Ladder, Liability-Driven |

Each category represents a fundamentally different philosophy about how to spend down a portfolio. By comparing methods across categories, you can understand which trade-offs matter most to you.

What Makes SafeWithdrawls Different

Bootstrap Sampling Instead of Monte Carlo

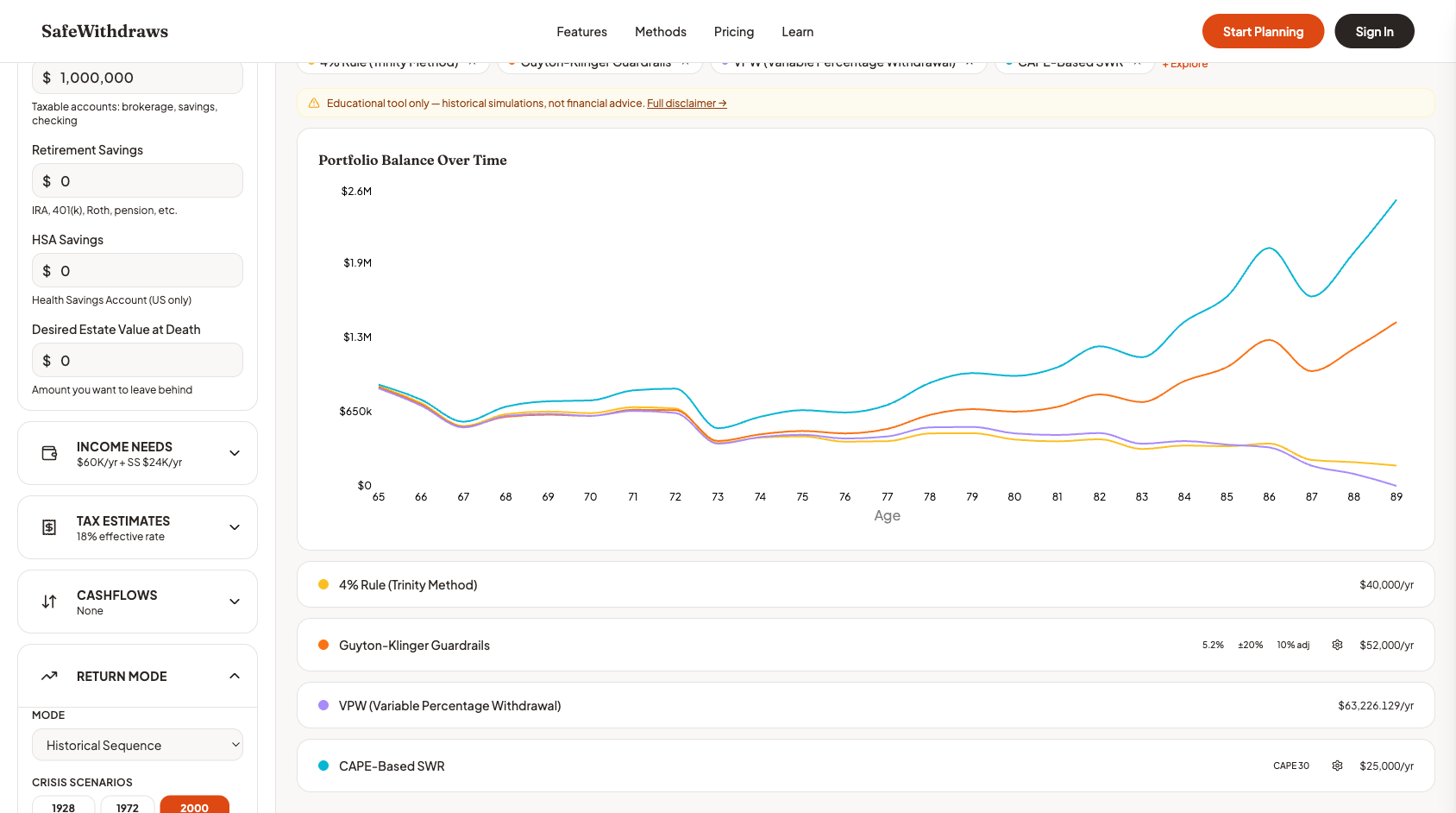

Most retirement calculators use Monte Carlo simulation, which generates random returns from a normal (bell-curve) distribution. The problem is that real markets do not follow a bell curve -- crashes are far more frequent and severe than a normal distribution predicts.

SafeWithdrawls uses bootstrap sampling, which draws returns directly from actual historical data (1928--2024). This preserves the fat tails, volatility clustering, and real-world correlations that Monte Carlo misses. Your projections are built from returns that actually happened, not from a simplified statistical model.

For a deeper explanation, see the Methodology page.

Crisis Scenario Testing

Beyond randomized simulations, you can test your strategy against specific historical crises:

- 1929 -- The Great Depression

- 1972 -- Stagflation and oil shocks

- 2000 -- Dot-com crash followed by the 2008 financial crisis

- 2008 -- Global financial crisis

- 2020 -- COVID-19 pandemic crash

These scenarios show exactly how your chosen strategies would have performed during the worst periods in modern market history.

Multi-Dimensional Success Metrics

Traditional calculators give you a single "success rate" -- the percentage of simulations where your portfolio survived. SafeWithdrawls goes further with two complementary scores:

- Portfolio Health -- Does your portfolio survive the full projection period? This measures longevity risk.

- Need Coverage -- Do your annual withdrawals actually meet your stated expenses? A strategy that keeps your portfolio alive but forces you to cut spending by 40% is not truly "successful."

The Overall Score combines both dimensions, giving you a more honest picture of how well a strategy actually serves your needs.

Important Disclaimers

SafeWithdrawls is an educational tool, not a financial advisory service. It does not provide personalized investment advice, and its projections are based on historical data that may not reflect future market conditions.

Before making retirement withdrawal decisions, consult with a qualified financial advisor who understands your complete financial situation. See our Terms and Disclaimer for full details.

Next Steps

- Quick Start Guide -- Learn how to use the Scenario Builder in five minutes

- Methodology -- Understand how bootstrap sampling works and why it matters

- Method Reference -- Explore all 23 withdrawal strategies in detail